101 / 148

101 / 148

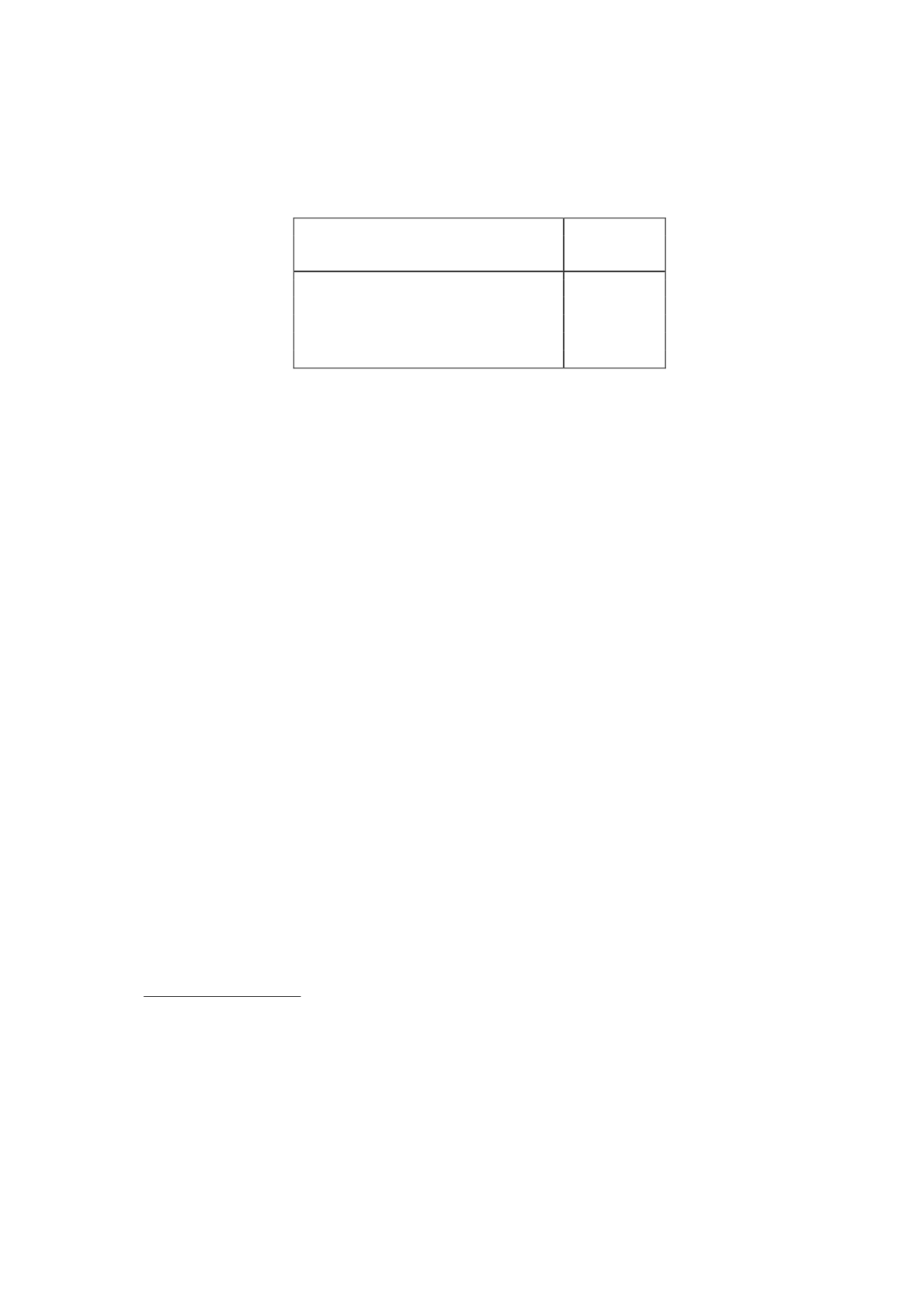

The Company depreciates its property, plant and equipment by the straight-line method at

annual rates based on the years of estimated useful life of the assets, the detail being as

follows:

Years of

estimated

useful life

Buildings

33

Plant

5 to 8

Computer hardware

3 to 5

Other fixtures

6 to 10

Other items of property, plant and equipment

6 to 10

Impairment of intangible assets and property, plant and equipment

At the end of each reporting period (for intangible assets with indefinite useful lives) or

whenever there are indications of impairment (for other tangible and intangible assets), the

Company tests these assets for impairment to determine whether the recoverable amount of

the assets has been reduced to below their carrying amount.

Recoverable amount is the higher of fair value less costs to sell and value in use.

In the case of property, plant and equipment, the impairment tests are performed individually

for each asset.

Where an impairment loss subsequently reverses (not permitted in the specific case of

goodwill), the carrying amount of the asset is increased to the revised estimate of its

recoverable amount, but so that the increased carrying amount does not exceed the carrying

amount that would have been determined had no impairment loss been recognised in prior

years. A reversal of an impairment loss is recognised as income.

4.3 Operating leases

Lease income and expenses from operating leases are recognised in income on an accrual

basis.

A payment made on entering into or acquiring a leasehold that is accounted for as an

operating lease represents prepaid lease payments that are amortised over the lease term in

accordance with the pattern of benefits provided.

The leases in which the Company is a lessor consist basically of facilities which the Company

has leased to companies in its Group.

4.4 Financial instruments

4.4.1. Financial assets

Classification -

The financial assets held by the Company are classified in the following categories:

a)

Loans and receivables: financial assets arising from the sale of goods or the rendering

of services in the ordinary course of the Company's business, or financial assets which,

not having commercial substance, are not equity instruments or derivatives, have

fixed or determinable payments and are not traded in an active market.