12

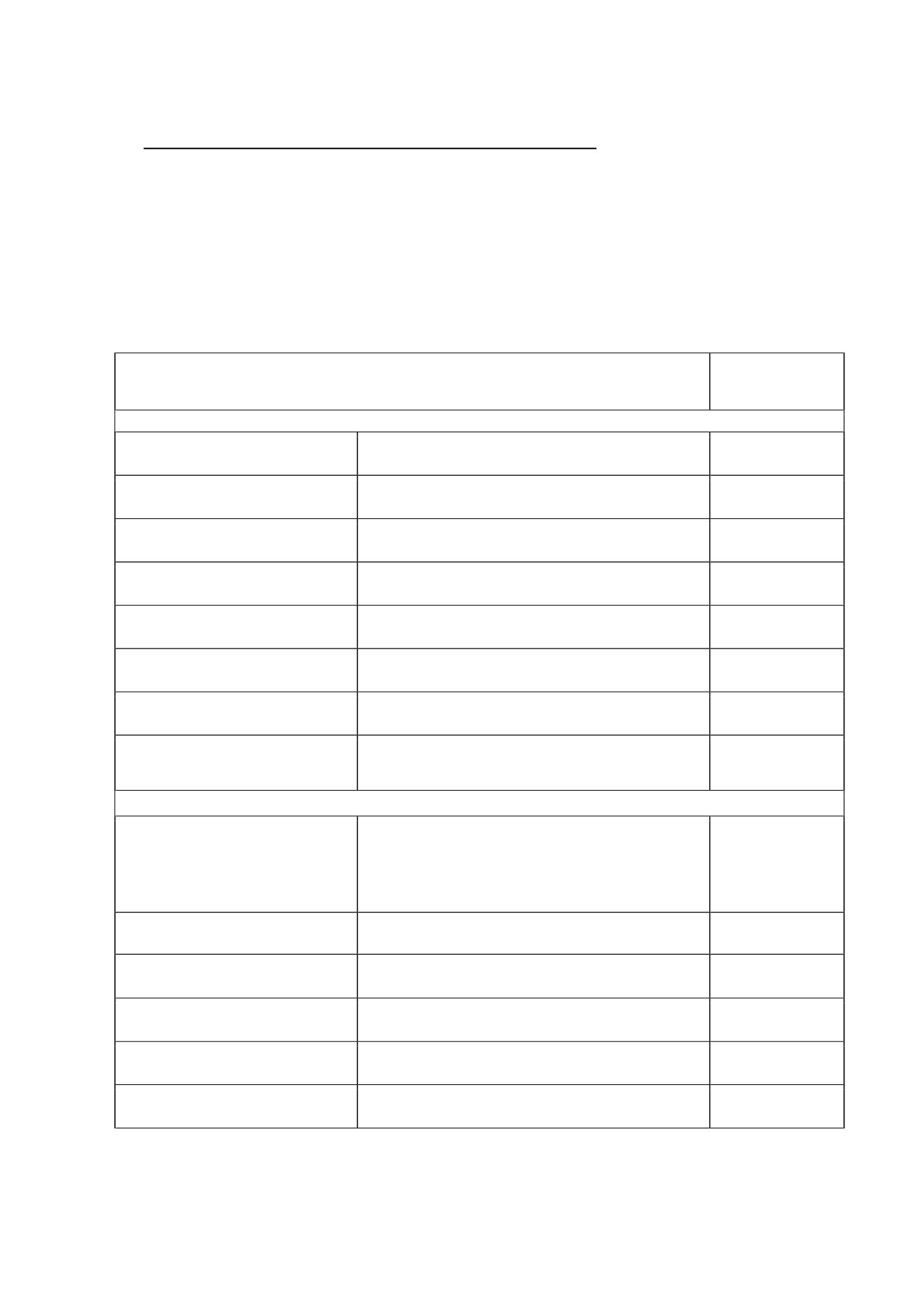

Standards and interpretations issuedbut not yet in force:

At the date of preparation of these consolidated financial statements, the most significant

standards and interpretations that had been published by the IASB but which had not yet

come into force, either because their effective date is subsequent to the date of the

consolidated financial statements or because they had not yet been adopted by the European

Union, were those listed below.

The directors have assessed the potential impact of applying these standards in the future and

consider that their entry into force will not have a material effect on the consolidated financial

statements.

New standards, amendments and interpretations:

Obligatory application

in annual reporting

periods beginning

on or after:

Approved for use in the EuropeanUnion

IFRS 10, Consolidated Financial Statements

(issued inMay 2011)

Supersedes the requirements relating to consolidated financial

statements in IAS 27

Annual reporting periods

beginning on or after 1

January 2014 (1)

IFRS 11, Joint Arrangements (issued inMay

2011)

Supersedes the current IAS 31, Interests in Joint Ventures

Annual reporting periods

beginning on or after 1

January 2014 (1)

IFRS 12, Disclosure of Interests in Other Entities

(issued inMay 2011)

Single IFRS presenting the disclosure requirements for interests in

subsidiaries, associates, joint arrangements and unconsolidated entities

Annual reporting periods

beginning on or after 1

January 2014 (1)

IAS 27 (Revised), Separate Financial Statements

(issued inMay 2011)

The IAS is revised, since as a result of the issue of IFRS 10 it applies

only to the separate financial statements of an entity

Annual reporting periods

beginning on or after 1

January 2014 (1)

IAS 28 (Revised), Investments in Associates and

Joint Ventures (issued inMay 2011)

Revision in conjunction with the issue of IFRS 11, Joint Arrangements

Annual reporting periods

beginning on or after 1

January 2014 (1)

Transition rules: Amendments to IFRS 10, 11 and

12 (issued in June 2012)

Clarification of the rules for transition to these standards

Annual reporting periods

beginning on or after 1

January 2014 (1)

Investment Entities: Amendments to IFRS 10,

IFRS 12 and IAS 27 (issued in October 2012)

Exception from consolidation for parent companies that meet the

definition of investment entities

Annual reporting periods

beginning on or after 1

January 2014

Amendments to IAS 32, Financial Instruments:

Presentation - Offsetting Financial Assets and

Financial Liabilities (issued inDecember 2011)

Additional clarifications to the rules for offsetting financial assets and

financial liabilities under IAS 32

Annual reporting periods

beginning on or after 1

January 2014

Not yet approved for use in the EuropeanUnion

IFRS 9, Financial Instruments: Classification and

Measurement (issued in November 2009 and in

October 2010) and subsequent amendments to

IFRS 9 and IFRS 7 on effective date and

transition disclosures (issued inDecember 2011)

and hedge accounting and other amendments

(issued in November 2013)

Replaces the IAS 39 requirements relating to the classification,

measurement and derecognition of financial assets and liabilities and

hedge accounting

Not yet defined (2)

Amendments to IAS 36 – Recoverable Amount

Disclosures for Non-Financial Assets (issued in

May 2013)

Clarifies when certain disclosures are required and extends the

disclosures requiredwhen recoverable amount is based on fair value less

costs to sell

Annual reporting periods

beginning on or after 1

January 2014

Amendments to IAS 39 - Novation of Derivatives

and Continuation of Hedge Accounting (issued in

June 2013)

The amendments establish the cases inwhich -and subject towhich

criteria- there is no need to discontinue hedge accounting if a derivative

is novated.

Annual reporting periods

beginning on or after 1

January 2014

Amendments to IAS 19 –Defined Benefit Plans:

Employee Contributions (issued in November

2013)

The amendments were issued to allow employee contributions to be

deducted from the service cost in the same period in which they are

paid, provided certain requirements aremet

Annual reporting periods

beginning on or after 1

July 2014

Improvements to IFRSs, 2010-2012 cycle and

2011-2013 cycle (issued in December 2013)

Minor amendments to a series of standards

Annual reporting periods

beginning on or after 1

July 2014

IFRIC 21, Levies (issued inMay 2013)

This interpretation addresses the accounting for a liability to pay a levy

that is triggered by an entity undertaking an activity on a specified date.

Annual reporting periods

beginning on or after 1

July 2014

(1) The European Union postponed themandatory effective date by one year. The original IASB application date was 1 January 2013.

(2) In November 2013 the IASB removed themandatory effective date of IFRS 9 and a new datewill not be set until the standard is complete. The new

date is not expected to be earlier than annual reporting periods beginning on or after 1 January 2017.